Most prices in an economy move in two directions as supply and demand forces change. Oil goes up, oil goes down. Apartment rental rates heat up, then they cool down. The value of a stock climbs, then it falls.

But wages are different. Wages have one gear, and that gear is upward.

This is one of the most fascinating properties of the labor market. Economists call it downward nominal wage rigidity, or more colloquially, "sticky down" wages. The idea is simple: when conditions change, pay almost always adjusts in the upward direction. It very rarely goes the other way, even when you'd expect it to.

I want to walk through why this happens, and then show you what it looks like in Pave’s market data, because the pattern is even cleaner than I expected.

Why wages resist going down

Standard supply-and-demand says that when demand for labor falls, the price of labor should fall to clear the market. In practice, that's not what happens. When demand drops, companies reach for layoffs and hiring freezes long before they reach for pay cuts. The pay of the people who remain stays put, or keeps climbing.

And this same anchoring shows up when people change jobs. Candidates rarely accept a step down in base pay to move, so a new offer usually has to meet or beat what someone already earns, which means the floor tends to travel with the worker from role to role.

There are a handful of well-understood reasons for this.

- Morale: Cutting someone's pay is one of the most demotivating things an employer can do. It doesn't just lower the cost line, it tanks productivity, poisons trust, and pushes your best people toward the door. The math almost never works.

- Contracts (both the written and the unwritten kind): Union agreements and employment contracts formally lock in salary levels. But the more powerful version is the implicit contract: the shared understanding between a company and its people that pay is a floor, not a variable that gets renegotiated downward every time the market wobbles.

- Legal: Minimum wage laws put a hard floor under a large slice of the labor market. You physically cannot adjust those wages down, no matter what the demand curve says.

- Strategic: A lot of companies deliberately pay above market to attract and retain the best talent. That premium becomes a baseline they won't cut, because cutting it defeats the entire reason they set it in the first place.

Put those four forces together and you get a market where the price of the single most important input, human labor, is structurally biased upward. There's genuinely no other market on the planet quite like it.

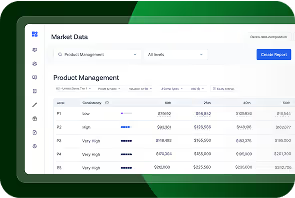

What Pave’s data shows

Theory is one thing. I wanted to see how strong the effect actually is in real compensation data, so our team looked across a consistent set of companies in Pave's dataset and asked a simple question: Of all the salary changes companies made, what share moved pay up versus down?

The answer was lopsided in every single quarter:

Across more than 11,000 analyzed companies in the United States, between 91% and 98% of all salary adjustments in any given quarter were increases. Decreases never accounted for more than 9%, and in most quarters they sat in the low single digits. There's some quarter-to-quarter noise in the exact figure, but the shape never changes. When a company touches an employee's salary, it's almost always raising it.

When does pay actually go down? Usually it's not a cut in the way you'd think. It's someone moving laterally into a different role, or shifting into a commission-heavy position with a lower base by design. The clean case of "we lowered this person's pay for the same job" is vanishingly rare.

Here's the consequence:

Look at aggregate base salaries over the same window. Across a consistent set of companies, average base salary climbed from roughly $146,800 to $163,600, and median base salary climbed from $140,000 to $155,200. That's a steady march up and to the right, and it happened straight through a stretch that included layoffs, hiring freezes, and a genuinely difficult market for large parts of tech and SaaS.

There's a lot of chatter right now about the market being K-shaped, a tale of two cities. You have the AI supernovas on one branch, and a lot of fear that everyone else is getting squeezed on the other. And it's true that headcount decisions have been brutal in places.

But headcount and wage level are two different variables. Companies froze hiring and ran layoffs. What they did not do, in the overwhelming majority of cases, was cut the pay of the people who stayed. The sticky-down property held.

Why this matters

The practical takeaway for anyone setting compensation is that a base salary is close to a one-way ratchet. Once you set it, you own it, in good markets and bad. That's worth internalizing, because it means every leveling and offer decision carries more permanence than a spot price would.

The bigger takeaway is about how you read the labor market. When the news is full of layoffs, it's easy to assume wages must be falling too. The data says otherwise. Employment levels are cyclical and can swing hard in both directions. But wage levels, for the population of people who remain employed, essentially don't. They compound upward.

This also reframes the role that compensation benchmarking plays in society. In a market where the real action is all on the upside, the question is never "will this employer cut," it's "who's willing to pay more to win the person." That competition works far better when both sides can see the terrain. A market where compensation is a black box is a market where good people get underpaid by accident and employers overpay out of fear, because nobody has a reliable read on what a role is actually worth.

Transparent, well-constructed benchmarks don't force anyone's hand; they just let raises and offers get made against real information instead of guesswork. In a market that's structurally biased toward raising pay, better information mostly helps the people getting paid.

Data throughout is drawn from companies participating in Pave's compensation dataset, presented as rolling 12-month averages across a consistent set of companies. Join Pave Data Lab for more analyses like this.

.avif)

Matt Schulman is CEO and founder of Pave, the complete platform for Total Rewards professionals. Prior to Pave, he was a software engineer at Facebook focusing on user-centric mobile experiences. A self-proclaimed "comp nerd," Matt is known for sharing data-driven thought leadership around all things compensation and personal finance.